Scenario 9

Contents

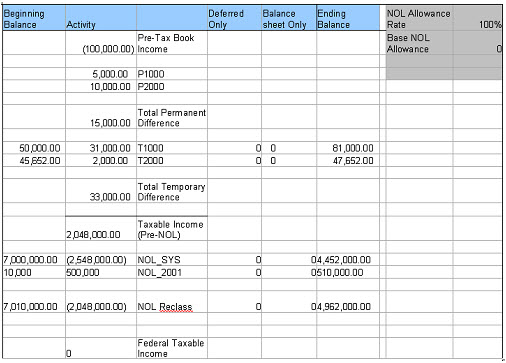

When the NOL Allowance Rate is set to 100%, the Base NOL Allowance to 0, and there is another NOL Temporary Difference with Activity (500,000), the NOL Reclass is the sum of 100% of the Federal Taxable Income (2,048,000.00) and the NOL Temporary Difference (500,000).

[(2,048,000.00) <Federal Taxable Income> + (500,000)< NOL TD>] – 500,000 <NOL TD> = - 2,048,000.00 <NOL Reclass>

If the NOL Reclass is added to the Federal Taxable Income (Pre-NOL), the Federal Taxable Income (Post-NOL) is 0.

2,048,000 <TI Pre-NOL> + -2,048,000 <NOL reclass> = 0 <TI Post-NOL>

NOL Ending Balance

(Beginning Bal + Deferred Only + Balance Sheet Only) + (NOL Reclass) = NOL End Bal

(7,010,000 <BBal> + 0<DO> + 0 <Bal O>) + (-2,048,000 <NOL Reclass>) = 4,962,000 <EB>