Scenario 8

Contents

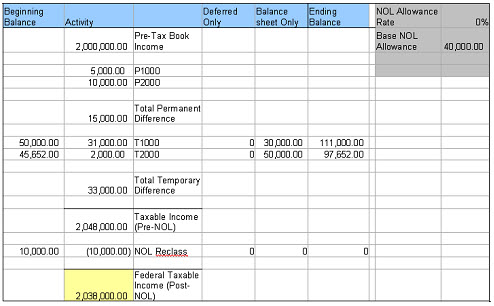

When the NOL Allowance Rate is set to 0% and the Base NOL Allowance is set to 40,000, the NOL Reclass is the total NOL Beginning Balance (10,000), because you cannot use more NOL than you have in the beginning balance.

(10,000 <NOL Beginning Bal> = -(10,000)<NOL Reclass>

If the NOL Reclass is added to the Federal Taxable Income (Pre-NOL), the Federal Taxable Income (Post-NOL) is 0.

2,048,000 <TI Pre-NOL> + -10,000 <NOL reclass> = 2,038,000 <TI Post-NOL>

NOL Ending Balance

(Beginning Bal + Deferred Only + Balance Sheet Only) + (NOL Reclass) = NOL End Bal

(10,000 <BBal> + 0<DO> + 0 <Bal O>) + (-10,000 <NOL Reclass>) = 0 <EB>

Note: The NOL Reclass takes the total NOL Beginning Balance because the Base NOL Allowance of the Federal Taxable Income (Pre-NOL) is greater than the available NOL Deferred Tax Asset.