Scenario 7

Contents

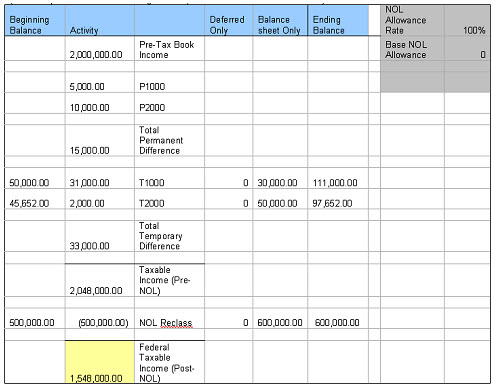

When the NOL Allowance Rate is set to 100% and the Base NOL Allowance is set to 0, the NOL Reclass is the product of the NOL Beginning Balance (500,000) and the NOL Allowance Rate (100%).

500,000 <NOL Beginning Bal> * 100% <NOL allowance rate>= -(500,000)<NOL Reclass>

If the NOL Reclass is added to the Federal Taxable Income (Pre-NOL), the Federal Taxable Income (Post-NOL) is 0.

2,048,000 <TI Pre-NOL> + -500,000<NOL reclass> = 1,548,000 <TI Post-NOL>

NOL Ending Balance

(Beginning Bal + Deferred Only + Balance Sheet Only) + (NOL Reclass) = NOL End Bal

(500,000 <BBal> + 0<DO> + 600,000 <Bal O>) + (-500,000 <NOL Reclass>) = 600,000 <EB>

Note: The NOL Reclass takes the total NOL Beginning Balance because 100% of Federal Taxable Income (Pre-NOL) is greater than the available NOL Deferred Tax Asset.